We just bought our first fix and flip renovation house. (If ya missed the big news, here is a YouTube video and a blog post all about it).

One of the things I find frustrating is when you are trying to plan or prepare for something and you can’t find real numbers on things because people aren’t willing to share. So, I want to help you and walk you through the numbers of purchasing our fix and flip house.

Because this was our first time purchasing a home, we didn’t really know what to expect. I knew there were other fees and things involved in buying a house other than the down payment, but I had no idea what they actually were.

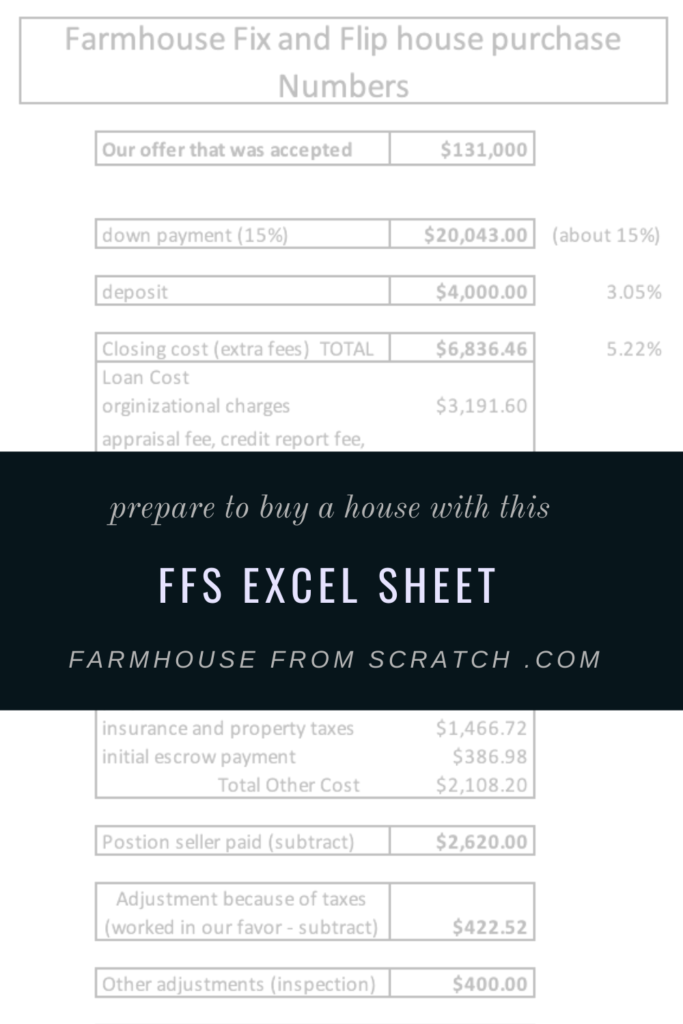

The house we bought is in central Washington in a rural area and is 2,263 square feet (3 bed & 2 full baths). The seller accepted our offer of $131,000. Which we felt was a really good deal for this area. Let me break down the cost of buying our new fix and flip.

Down Payment

The first thing we have is our down payment. If it’s the home you are going to be living in you can get your down payment lowered – but because we were buying an investment house and not living in it right away, the lowest we could pay for our down payment was 15% which is $20,043.

TOTAL DOWN PAYMENT: $20,043

Deposit

When we made our offer we put down a $4,000 deposit – we had to have that money 2 or 3 days after the offer was made and accepted. In the end, they take the $4,000 out of the total.

TOTAL DEPOSIT: $4,000

Closing Cost (Extra Fees)

Beyond the down payment they broke the costs down into 2 sections: Loan cost & other costs.

Side note: If we were paying for this house in cash then our fees would be significantly lower. Because this is an investment house for us, we wanted to pay the least amount up front so that we had extra cash to pay for our upgrades and renovations.

Loan Costs = $4728.26

Under our loan costs, we have origination charges that equaled $3,191.60. There were appraisal fee, credit report fee, flood certificate fee which came out to $778.50. There were a whole bunch of fees to the title company like reporting, escrow, sales tax, title insurance, notary fee and settlement fee in $758.16.

Other costs: $2,108.20

Taxes and other government fees that came out to $254.50. There were pre-paids like home owners insurance and property taxes which equaled $1,466.72 There was an initial escrow payment $386.98 which had to be paid at closing.

So if we add the loan and other costs, that would get us our total extra fees. This is the total of the additional fees on top of our down payment. So not only did we have to have the down payment which was about 15% of our offer, but we also had to have enough for the extra fees which was about 6% of our offer (plus a couple others items of business coming up).

TOTAL CLOSING COST: $6,836.46.

Are you lost yet? All the numbers and paperwork can be extremely confusing and frustrating. Let me save you from some of the frustration okay? Alright, back to the numbers and stuff.

Something we did in our loan (because we wanted initial cash needed up front to be the lowest possible – so we had as much extra cash leftover to fix the house) we changed our offer later to a higher number, but asked the seller to pay some of our fees. It didn’t change the actual amount the seller was receiving – but it made it so we could lump more costs into our loan so we didn’t have to pay as much upfront. It changed our cash needed upfront to close by about $2,000.

There were some last minute adjustments with taxes that actually credited us $422.52. And the seller agreed to pay part of the fees which came to $2620

So lets play it back and add it all up:

(Total closing costs) + (down payment of 15%) – (deposit since we already paid it) – (portion seller agreed to pay) – (our tax adjustments) = (amount needed to officially close in the office)

$6,836.46 + $20,043 – $4000 – $2620 – $422.52 = $19,836.94

When we went to the office to close we had to pay a total of $19,836.94

The only other fee we had to pay between making our offer and closing on the house was the inspection fee. We were there for the inspection and had to pay the inspector directly and that was $400.

If you aren’t sure about an inspection we highly recommend reading this article. We paid the average inspection cost of $400. The cost of the inspection varies based on the square footage of the house, the age, any problems with the house, and more.

Add it all up for a GRAND TOTAL of $24,236.94. This was the amount we needed in cash to actually buy the house. Below is an excel image of all the calculations – for those who like to see the numbers line up!

I know it might seem inappropriate to share money facts like this that are super specific, but how is anyone supposed to plan to buy a house when they have no idea how much it is actually going to cost?

I have created an excel sheet sharing all the information above in a more easy to read format plus another sheet where you can make a rough estimate of how much money you might need upfront to buy your home. This isn’t a perfect math because there are way too many variables, but we did some research and learned that our numbers were close to average.

If nothing else, we hope this can give you the confidence to plan for your dream – whether it’s buying a home or building one, planning is extremely important.

You’ve gotta know the numbers to be able to plan! So I hope this helps you understand the process of buying a house a little more and have the courage to find what you are looking for!

If you have any other questions about buying a house let us know and we will see if we can answer them!

~Farmer’s Wife

Leave a Reply